.The Board of Directors has implemented a Risk Management Policy which establishes the overall Risk Management Framework for managing operational risk. Specifically, the Risk Management Policy aims to:

- Contribute to profitable prudential performance by achieving an appropriate balance between realising opportunities while minimising losses.

- Maintain a comprehensive and up-to-date Risk Appetite Statement that addresses all material risks and sets the risk limits acceptable to the Board.

- Be concerned with risk as exposure to the consequences of uncertainty, or potential deviations from that which is planned or expected.

- Address Capital Management.

- Facilitate regular reporting to Senior Management, the Board and relevant committees.

Risk Management Framework

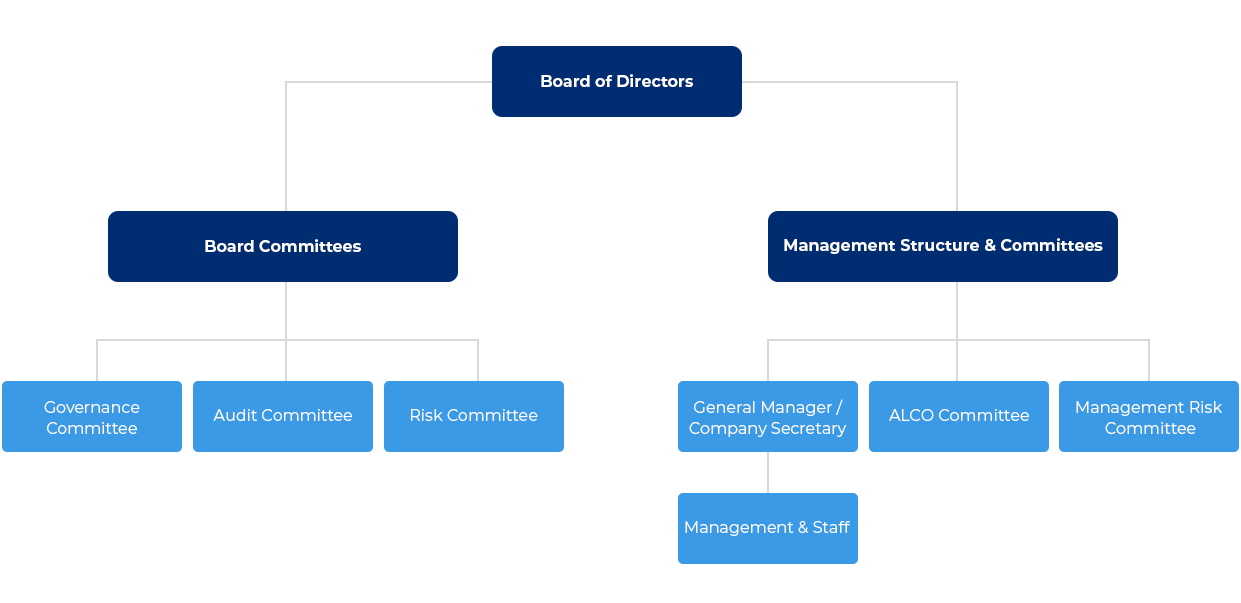

The Board of Directors has overall responsibility for the establishment and oversight of the risk management framework. The Board has established separate Audit and Risk Committees which are responsible for developing and monitoring risk management processes. The committee reports regularly to the Board of Directors on its activities.

Risk management policies and procedures are established to identify and analyse the risks faced by Geelong Bank, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management processes and systems are reviewed regularly to reflect changes in market conditions and Geelong Bank’s activities.

The Audit and Risk Committees oversee how management monitors compliance with Geelong Bank’s risk management policies and procedures and reviews the adequacy of the risk management framework in relation to the risks faced by Geelong Bank. The Audit and Risk Committees are assisted in its oversight role by Internal Audit. Internal Audit undertakes regular reviews of risk management controls and procedures, the results of which are reported to the Audit & Risk Committees.

Geelong Bank has undertaken the following strategies to minimise risks.

Market Risk

The Bank is not exposed to currency risk, and does not trade in the financial instruments it holds on its books.

Credit Risk - Loans

The risk of losses from the loans undertaken is primarily reduced by the nature and quality of the security taken. The Board policy is to maintain at least 85% of loans in well secured residential mortgages which carry an 80% Loan to Valuation ratio or less.

The Bank has a concentration in the retail lending for members who comprise employees and family in the Ford Motor Company. This concentration is considered acceptable on the basis that the Bank was formed to service these members, and the employment concentration is not exclusive.

Should members leave the industry the loans continue and other employment opportunities are available to the members to facilitate the repayment of the loans.

Credit Risk - Liquid Investments

The risk of losses from the liquid investments undertaken is reduced by the nature and quality of the independent rating of the investee and the limits to concentration in one entity.

The Board policy is that investments shall be widespread to avoid any undue concentration of risk and all investments must be with financial institutions with a rating in excess of BBB- or higher.

Credit Risk - Equity Investments

All investments in equity instruments are solely for the benefit of service to Geelong Bank. Geelong Bank invests in entities set up for the provision of services such as IT solutions, treasury services etc where specialisation demands quality staff which is best secured by one entity.

Liquidity Risk

Geelong Bank has set out the maturity profile of the financial assets and financial liabilities, based on the contractual repayment terms.

Geelong Bank is required to maintain at least 9% of total adjusted liabilities as liquid assets capable of being converted to cash within 48 hours under the APRA Prudential standards. Geelong Bank's policy is to apply 15% of funds as liquid assets to maintain adequate funds for meeting member withdrawal requests. The ratio is checked daily. Should the liquidity ratio fall below this level the management and the Board are to address the matter and ensure that the liquid funds are obtained from new deposits and borrowing facilities available.

Operational Risk

Operational risk is the risk of direct or indirect loss arising from a wide variety of causes associated with Geelong Bank's processes, personnel, technology and infrastructure, and from external factors other than credit, market and liquidity risk such as those arising from legal and regulatory requirements and generally accepted standards of corporate behaviour.

Geelong Bank’s objective is to manage operational risk so as to balance the avoidance of financial losses and damage to Geelong Bank’s reputation with overall cost effectiveness.

Facebook

Facebook LinkedIn

LinkedIn Instagram

Instagram